Ever since I have started writing my blog and recording my podcasts and sharing them with my near and dear ones, a lot of people do come up to me and discuss their investments and have started asking me to review their portfolio and are seeking financial planning advice.

Just last week, I bumped into one of my father’s friends in my office building and he invited me to his office for a cup of chai. The conversation swiftly moved to him discussing his plan to retire. He is 59 years old and wants to retire within a year or two, has a substantial amount in current investments and wanted to create a financial plan for his capital for him and his wife as he moves into the next phase of his life.

This prompted me to come up with a financial plan for him. Assuming he retires in a year, at the age of 60 with a capital of ₹2,00,00,000. Although the average life expectancy in Urban area in India is 70 years I am going to create a plan till the age of 80.

Assumptions

Capital: ₹2,00,00,000

Debt Allocation: 65%

Equity Allocation: 35%

Tenure of Plan: 20 years

Debt Returns: 7% (liquid funds)

Equity returns: ~12% – Since this planner is based on assumptions, I did want to use some real numbers. For equity returns I have linked the annual returns of BSE SENSEX of the last 20 years. (A SENSEX index fund)

Annual Withdrawals: ₹1,00,000 per month = ₹12,00,000

Exceptional Expense: Every third year, an expense of ₹6,00,000 is incurred and this expense increases by ₹ 1,00,000 at every occurrence (i.e. every third year).

The plan is to withdraw from the debt side of the portfolio. By investing in a liquid fund, the 7% return is closest it can be to risk-free and with a 65% debt allocation, this assures enough funds are available for withdrawal from this asset class without any exit load.

At the end of the year, adjust the debt-equity ratio back to 65%-35%. This will ensure that the debt side is not getting depleted Y-o-Y.

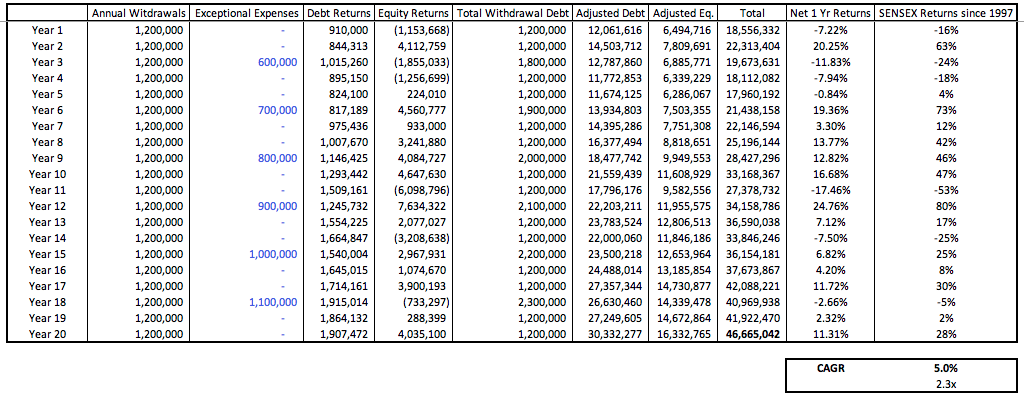

Based on above assumptions, at the end of the 20th year, the plan results in a net CAGR of 5.0% and 2.3x multiple on the initial capital. This is inclusive of all the withdrawals and exceptional expenses.

I have not shown any tax liabilities as the couple will be a retired couple, and withdrawals of ₹12,00,000 at 7% returns is an income of ₹84,000 hence not liable to tax. In the later years when there are larger withdrawals, the tax liability will be minimal due to benefit by indexation on the returns.

See below table:

According to me the important part of a financial plan is not the returns but the monthly withdrawals and expenses which have to be in check. If is important to spend within one’s means and establish a lifestyle accordingly.

If in the above assumptions and table, I increase the monthly withdrawals to ₹1,67,000, you will be left with a balance of -₹16,000 at the end of year 20 with a CAGR of -169%.

In exceptional expenses, there is more room to maneuver and one can go reasonably beyond the budgeted expense and still not lose their initial principal. If we increase the exceptional expense to ₹10,00,000 instead of ₹6,00,000 and increase by ₹1,00,000 at every subsequent occurrence of the expense, the CAGR is still a healthy 4.1% with a 2x multiple at the end of year 20.

See table below:

By keeping fixed expenses and living within an affordable lifestyle one can earn from saved up capital and still spend higher amount on an annual basis for any unforeseen expenses, be it for health, or foreign trips or purchasing a new vehicle or getting house repairs done, one can still preserve initial capital if monthly expenses are controlled.